By Gary Aiken | October 9, 2025

“Alternative Facts,” “Post-Truth,” and “Trust Crisis” are all popular buzzwords that attempt to describe American politics in the modern era of social media dominance. That device in your hand, where most Americans get their daily “news” from, may be more influential than you realize. The algorithms embedded in Facebook, Instagram, YouTube, X, and TikTok are designed to show you content that you’re most likely to engage with, which can influence how you think and feel. They prioritize emotional triggers—what you enjoy, what enrages you, and what you long for nostalgically—over rational information.

In the past, investors have clung to an idea of leading and lagging indicators to assess the direction of the U.S. economy. The Conference Board, a non-profit market research think tank, publishes a monthly index of leading indicators. These indicators are broken into financial and non-financial components. The financial components are things I write about frequently: the stock market, credit markets, and interest rate spreads. The non-financial components include topics I often cover, like weekly jobless claims and consumer expectations, as well as others I haven’t written about recently, such as new purchase orders, building permits, and hours worked in a work week.

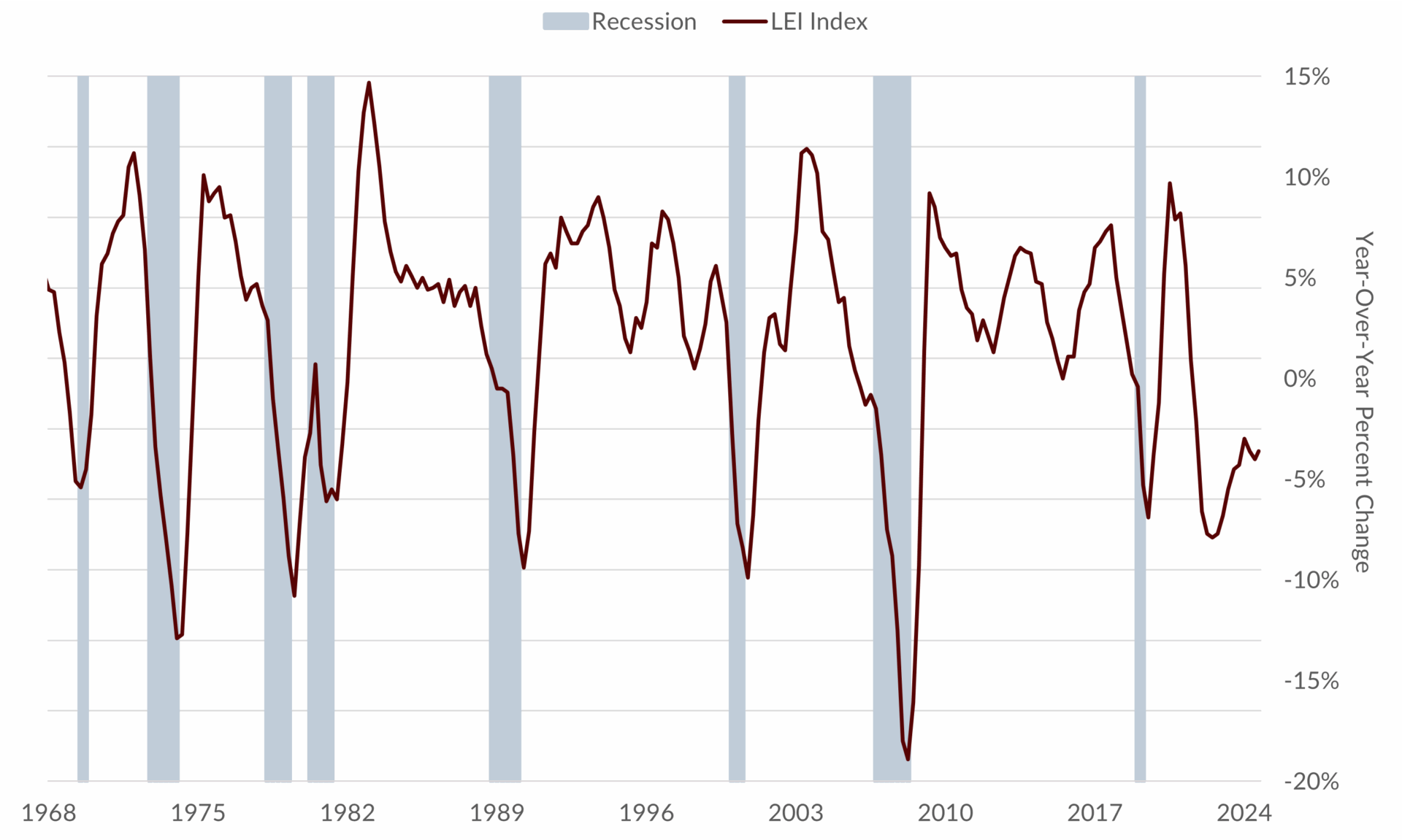

Since 1968, a year-over-year percentage decline in the Index of Leading Economic Indicators (LEI) has coincided with a recession. Curiously, in Spring 2023, the LEI index registered an -8% year-over-year decline, plummeting from the post-Covid highs and marking what should have been the start of a recession. And yet, the recession never came. Why?

Declining Leading Indicators Have Forecasted Recessions

Source: Bloomberg Finance, L.P.

The 2023 LEI trough was most like the 1980-82 period. Facing the most significant inflation in a generation, the Federal Reserve increased rates from zero to 5.25% very quickly, intending to quash inflation and perhaps trigger a recession. The recession never came. The Powell Federal Reserve and the Biden Administration acted very differently from the Volker Fed and Reagan White House.

Although it was raising short-term interest rates, the Powell Fed continued to provide accommodation to the economy through the purchasing of bonds and mortgages (quantitative easing). When a banking crisis arose from inverted interest rate spreads (an LEI component), the Fed and Federal government chose to bail out failing banks by changing accounting rules and providing cash to hide massive unrealized losses. Congress continued to increase spending and the White House used the Covid-crisis to create moratoriums on mortgages and student loan payments diverting attention from and offsetting the weaking position of markets and manufacturers. Finally, the Biden administration welcomed millions of immigrants into the United States and gave them massive amounts of government assistance. We should have had a recession, but the monetary and fiscal authorities acted together to insulate the labor market from the contraction necessary to subdue inflation.

That’s not where the story ends. The LEI index read -3.6% in August 2025. We ought to be in a recession today, and yet we are not. Credit, interest rate, and stock market conditions have been improving. Consumer expectations, new manufacturing orders, and housing building permits are what is driving the LEI Index’s negative position.

Manufacturing has been declining here in the U.S. for decades. The ISM New Orders Index, another negative LEI component, has been in contraction since 2022, but manufacturers only account for about 8% of total jobs in the U.S., making it less relevant than it once was. Also, the advancement of Artificial Intelligence will likely lead to increased manufacturing productivity and, when combined with tariff-induced onshoring, may drive the ISM component into expansion territory.

Finally, building permits will tend to reflect supply and demand for new housing units and the financial conditions around buying a new home. Housing prices are starting to decline in several major metropolitan areas as demand wanes. At the same time, interest rates are likely to decline further, maybe making affordability greater.

It is amid this backdrop that a negative LEI Index doesn’t necessarily mean a recession. The Powell Fed is conceding that the path ahead is for easier financial conditions. The Fed is reluctantly working hand-in-hand with the Trump fiscal authority. Recent legislation is about to drop significant stimulus on businesses and consumers. We may each follow our own set of alternative facts, but as an investor and economist, I cling to the founding assumption of microeconomics—that individuals are rational actors when it comes to money. I watch what really matters: Do consumers have cash to spend? Do businesses need to cut costs or invest in their future for profit? Signs point to a continued expansion, not a recession.

Author

Gary Aiken, Chief Investment Officer

Gary Aiken is the Chief Investment Officer for Concord Asset Management and is responsible for macroeconomic analysis, asset allocation, and security selection, as well as trading and investment operations.

Gary has over 23 years of investment experience and holds an undergraduate degree in economics from the University of Maryland and an MBA from The George Washington University School of Business.

—

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Concord Asset Management, or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Concord Asset Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Concord Asset Management is neither a law firm, nor a certified public accounting firm, and no portion of this content should be construed as legal or accounting advice. A copy of Concord Asset Management’ current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.concordassetmgmt.com. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please remember to contact the firm in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, and/or revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Concord Asset Management and Concord Wealth Partners shall continue to rely on the accuracy of information that you have provided. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.