By Gary Aiken | May 7, 2026

A few months ago, several private software companies defaulted on their debt covenants. This caused many lenders to software companies to reevaluate their borrowers’ ability to pay. When lending, there’s an adage – the return OF the principal is more important than the return ON the principal. This means lenders are always examining the assets of a borrower in a foreclosure and their ability to pay debt service (principal and interest) for the term of the loan.

The software business has been, for the most part, an excellent one for the past 30 years. While not without internal disruption, many software companies have had wonderful profitability and wide moats. A piece of software requires a lot of upfront costs – gathering requirements, coding, testing, and selling the use case. Once created, the costs of replication are near zero and your customers tend to be long term – requiring updates, add-ons, and ancillary services and customizations.

Acquiring software has a lot of costs for businesses, too. The search process is long and cumbersome, involving consultants and a considerable amount of internal stakeholders’ time. Once bought, it’s usually very difficult to change – even if it isn’t working out as expected. Inertia creates a feeling of “It doesn’t do everything we want, but it does enough and changing would be difficult and we couldn’t guarantee success”. Software companies know this and offer just enough support to prevent changing.

Further, the business model has changed over the years from being sold as a one-time purchase. Most software today is sold “in the cloud” as a subscription based upon usage and tiers of customization. This model delivers predictable, recurring revenue to software companies and predictable, recurring costs to their customers.

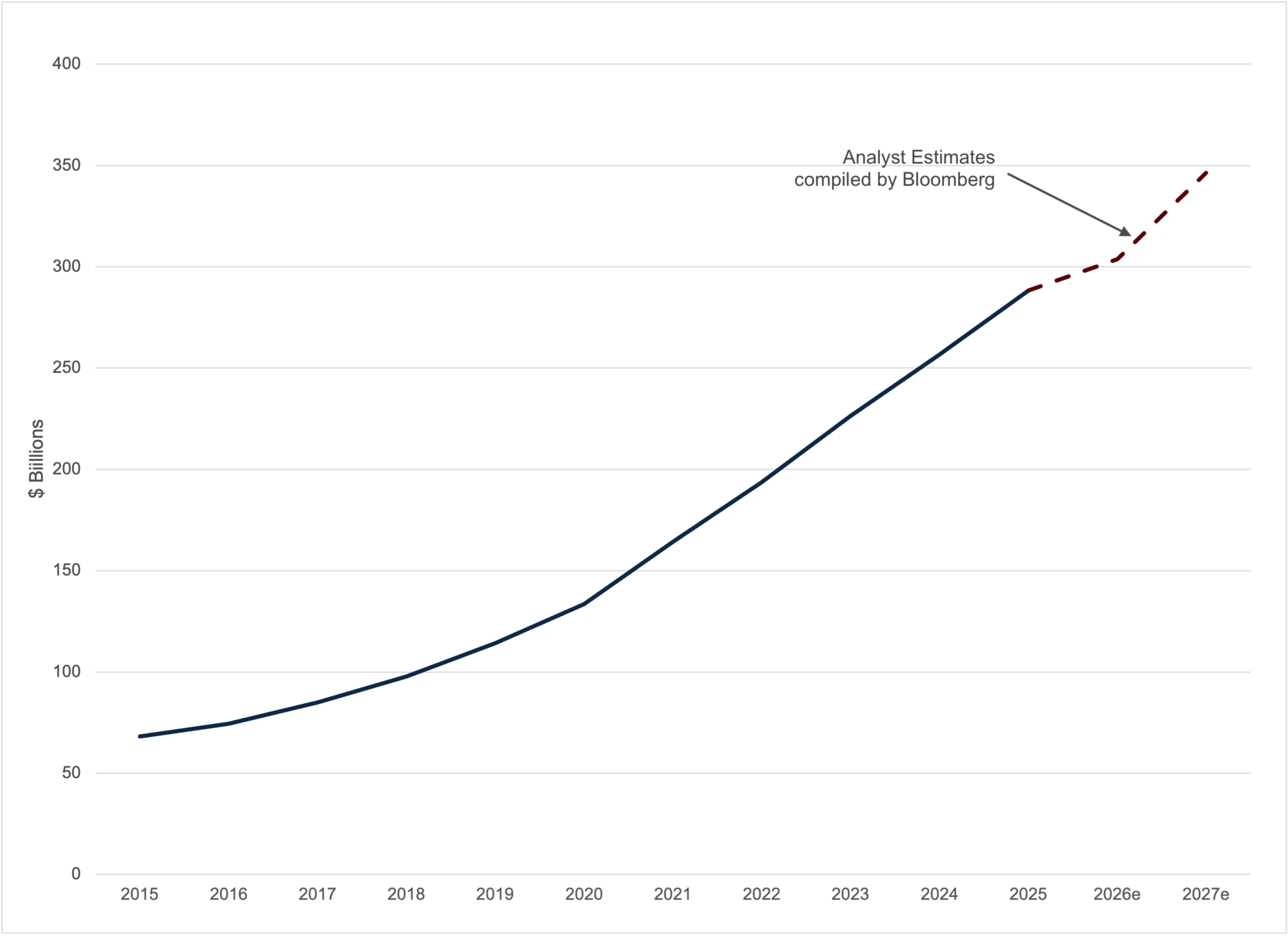

Over the past five years, revenues at publicly traded software companies included in the S&P North American Expanded Technology Software Index have increased revenues by 20.1% per year on average to over $288 billion. This excludes Microsoft, Oracle, and Palantir. Gross margins have remained steady at about 73%. The software business has been very profitable.

To succeed in business, you need to do three things: increase revenues, cut costs, and invest wisely. For software companies, increasing revenues are about to become much more difficult and for their customers, bringing software development in house is about potentially cutting costs, dramatically. The disruptor is AI. Software development is being democratized, and the cost of investment is going down. As such, analysts are already reducing future revenue growth estimates for software firms. The 20% per year plug-in has been reduced to 14.8% and may drop further.

Software Revenues

Source:Bloomberg Finance, LP.

Evaluating winners, survivors, and losers in the software industry will be very difficult. We have questions to ask on the software side. Whose businesses are so sticky that the sheer amount of pain to change will provide a sustainable moat? Are “systems of record” (software that stores crucial business data) enough to keep clients from developing their own? Which companies will use AI themselves to reduce headcount without sacrificing quality? Which companies will convert AI from a problem to a solution for their customers? Who will invest in customer service that builds trust, rather than take it for granted? What will be the resulting new growth rate for revenues and gross margins? If lower, what price should investors pay for that company’s stock?

Evaluating from a software buyer’s side, how can I use AI to replace entirely something that has been a headache for years? It seems crucial to remember the time dimension. Companies often run legacy software side by side when installing a new system. This stealth “leaving before leaving” may catch some software companies by surprise, when large accounts “suddenly” disappear.

As always, rewards demand their share of risk. Investors in software – both equity and debt – need to be wary of management promises in an era of disruption.

Note: Data is based upon exchange listed companies who are holdings in the iShares Expanded Tech-Software Sector ETF (IGV). Chart data excludes Microsoft, Oracle, and Palantir at Concord’s discretion. Percentage figures for gross margin and revenue growth rates are based upon the 2025 revenue weighted average positioning within the ETF, excluding Microsoft, Oracle, and Palantir.

Author

Gary Aiken

Chief Investment Officer

Concord Asset Management

Gary Aiken is the Chief Investment Officer for Concord Asset Management and is responsible for macroeconomic analysis, asset allocation, and security selection, as well as trading and investment operations.

Gary has over 23 years of investment experience and holds an undergraduate degree in economics from the University of Maryland and an MBA from The George Washington University School of Business.

—

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Concord Asset Management, or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Concord Asset Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Concord Asset Management is neither a law firm, nor a certified public accounting firm, and no portion of this content should be construed as legal or accounting advice. A copy of Concord Asset Management’ current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.concordassetmgmt.com. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please remember to contact the firm in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, and/or revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Concord Asset Management and Concord Wealth Partners shall continue to rely on the accuracy of information that you have provided. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian