By Gary Aiken | April 2, 2026

I write these monthly letters to you without the help of Artificial Intelligence. Of course, we use AI afterwards for several important purposes. Among other things, it generates possible headlines, social media optimizations, and it summarizes the text to ensure that the machine and I agree that the takeaways match my intent. As we come to the end of the fourth week of hostilities in the Middle East, investors really could use an AI that helped make sense of what we think is going on.

I’m going to avoid talking about the military, political, and potential outcomes of the war itself in this letter. It’s a cop out for sure, but I’m not sure that I have the expertise, imagination, or the necessary gumption to claim some knowledge you can’t get elsewhere. I am going to talk about what has happened to asset prices and what our framework for evaluation of risk and reward going forward might be.

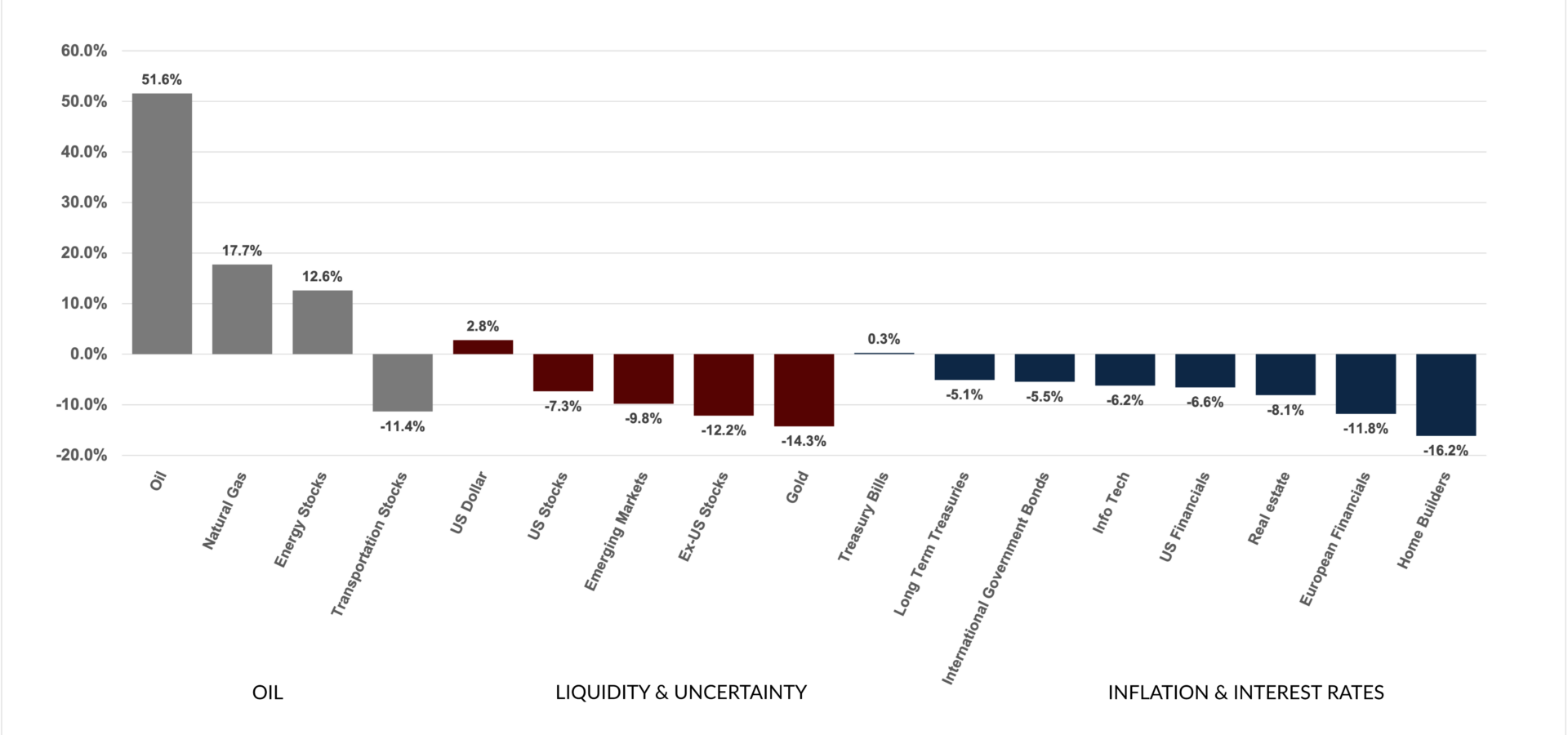

The war began on Saturday, February 28. And the chart of the month shows some of the moves among asset classes and sub-asset classes, through March 28. I’ve divided these into three categories. First, beneficiaries of the spike in the price of oil and natural gas. Second, examples of uncertainty and liquidity. Third, inflation and interest rate related moves.

The War Effect on Selected Returns in Three Categories

Source:Bloomberg Finance, LP.

In the Oil section, I’ve included the price of oil, the price of natural gas, energy stocks, and transportation stocks. You could also throw most agricultural commodities into this basket, and they would be up in price since the war began as well. There is no doubt that the extreme limiting of passage through the Strait of Hormuz has had a severe effect on the ability to transport oil out of the Persian Gulf. The Houthis, an Iran-aligned tribal proxy group in Yemen, is threatening to limit transport out of the Red Sea into the Indian Ocean. Trapping tankers makes tankers scarce. Nearly 20% of global oil supply and 25% of natural gas liquids and fertilizer components are cut off from destination. Even if the war ended today, it would be months before transportation could be caught up and perhaps years before destroyed facilities could be back online.

It is important to think about how the war might end. If the War ended with a friendly regime in Tehran, oil might be able to go back to pre-war prices or lower. If the War ends in any other state, with the existing regime and its proxies able to somewhat control, toll, or threaten the passage of tankers through the Persian Gulf and Red Sea, then it could be that oil stays significantly elevated indefinitely.

Which takes me to the second grouping – Liquidity and Uncertainty. We have seen an almost normal reaction to this global crisis with risk assets selling off. US stock markets, developed markets outside the US, and emerging markets are all down. Virtually every sector is down, except for energy stocks, which leads me to the general conclusion that investors who were too bullish going into this event have had to pair back as selling begets more selling. The mysterious downdraft in the price of gold also smells like it has more to do with liquidity than anything else. If you’re an investor needing quick liquidity, gold ETFs are a good place to start considering how much money has been made recently. If you’re a country that needs to acquire gasoline and oil now at any price, selling gold may work. And if you’re a central banker, defending against a major decline in your currency, selling gold also helps.

The question is, who is the buyer on the other side? It would seem to me that the answer is whoever is trading dollars. The dollar has been appreciating versus other currencies and versus gold during this crisis – a normal reaction. For the past few years, I’ve been defending the dollar’s status with facts, not feelings, and those facts have proven correct so far. One additional aside that provides a decent segue to the last section, if I may. The dollar strengthening and the Supreme Court decision to take away the power of the President to impose tariffs are both disinflationary for US consumers.

Our final grouping is Inflation and Interest Rates. Remember 2022? Interest rates went up, stocks went down. Hardest hit were companies with high price to earnings ratios. I have written before that if interest rates are going up for the right reasons – real growth, productivity – then stocks can go up right with them. That was our thesis to start 2026. Since February 28, though, interest rates have been going up for the wrong reasons – deficits, debt, and inflation. And the US is not alone. As interest rates have gone up, long bonds, financials, high priced tech stocks, and interest sensitive home builders have all had large pullbacks.

Looking forward, there will be re-pricings. The longer the war drags on, the more global risk assets will sell off. The world still depends on energy and energy assets. For net energy exporters like the U.S., the crisis won’t be as severe, but the world is full of interdependencies, and the unknown or lesser-known connections will become better known as shortages and bottlenecks appear. These will be surprises and certain companies and sectors will sell off in sympathy.

At the same time, analysts have not yet begun to cut earnings estimates for U.S. companies, the AI capex buildout continues unabated, and every day, AI becomes more valuable to the productivity of global business. Industrial buildout and the rise of commodity prices will likely induce more spending on reshoring and friendshoring. The tax policy passed in the OBBBA last year will make that spending more palatable. The labor market in the U.S. is still very strong and net immigration is significantly lower than in previous years making labor scarce. A strong dollar makes imports cheaper and oil profits greater.

I have been writing that we have been sector neutral because of valuation, overweight US because of the relative strength of US companies, and short in duration to keep our bond powder dry when stock prices become attractive. Every day, stocks become more attractive and the list of great companies trading at attractive levels to cash flow grows. When the war ends, we will be ready buyers.

Footnotes

28-Day Returns: Oil (USO) +51.6% | Natural Gas (FCG) +17.7% | Energy Stocks (XLE) +12.6% | Transportation (XTN) -11.4% | US Dollar (UUP) +2.8% | US Stocks (SPY) -7.3% | Emerging Markets (SPEM) -9.8% | Ex-US Stocks (EFAX) -12.2% | Gold (GLD) -14.3% | Treasury Bills (BIL) +0.3% | Long Treasuries (SPTL) -5.1% | Int’l Gov Bonds (BWX) -5.5% | Info Tech (VGT) -6.2% | US Financials (XLF) -6.6% | Real Estate (VNQ) -8.1% | European Financials (EUFN) -11.8% | Home Builders (XHB) -16.2%

Author

Gary Aiken

Chief Investment Officer

Concord Asset Management

Gary Aiken is the Chief Investment Officer for Concord Asset Management and is responsible for macroeconomic analysis, asset allocation, and security selection, as well as trading and investment operations.

Gary has over 23 years of investment experience and holds an undergraduate degree in economics from the University of Maryland and an MBA from The George Washington University School of Business.

—

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Concord Asset Management, or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Concord Asset Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Concord Asset Management is neither a law firm, nor a certified public accounting firm, and no portion of this content should be construed as legal or accounting advice. A copy of Concord Asset Management’ current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.concordassetmgmt.com. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please remember to contact the firm in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, and/or revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Concord Asset Management and Concord Wealth Partners shall continue to rely on the accuracy of information that you have provided. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.