By Gary Aiken | June 4, 2026

The April 2026 Consumer Price Index for all urban consumers (CPI-U) reached 3.8%, the highest since May 2023. The Federal Reserve’s preferred inflation measure, Core Personal Consumption Expenditures (PCE) index reached 3.3%, the highest since November 2023. While these readings are certainly lower than the inflation seen during the post-pandemic easy money flood, for Core PCE, they are higher than most readings going back to the first Gulf War. Inflation readings at or near these levels in the past have been associated with the beginning of Federal Reserve hiking cycles.

And yet, incoming Federal Reserve Charman Kevin Warsh may decide to guide the Open Market Committee to “look through” the food and energy inflation driving CPI and PCE inflation higher. This may not be a mistake. Energy prices have risen 17.5% year-over-year through April due to the extended conflict in the Middle East. As of May 31, West Texas Intermediate Crude Oil was at $91 per barrel and Brent (a more global benchmark) was $94. These are up significantly from the $60 level seen in December. These numbers are lower than the peak conflict prices near $120 per barrel but also reflect some near-term demand destruction and about 50 million barrels released from the Strategic Petroleum Reserve since the end of March.

These energy price shifts have slowed economic growth around the world and have a similar effect to the purpose of hiking interest rates – to slow an overheated economy. However, given the cause of the spike, it’s unclear that raising interest rates would do much to lower the price of oil and energy commodities.

Similarly, food prices have been rising. Initially tariffs and then the related costs of energy price increases have been the main culprits of late. But over the past 15 years, U.S. food prices have risen by about 3% annually – only slightly above the average rate of inflation. Indeed, despite being excluded from CPI in Core because of its “volatile” nature, food has been between 13% and 14% of the basket steadily.

Raising rates might not cut down on food or energy costs, but it would certainly have an impact on slowing the engine of growth – services. Core services inflation is where the action is in the fight against inflation. Unfortunately, that’s also where all the economic growth is coming from, too. The AI revolution providing jobs, building factories, and raising blue-collar wages is also causing scarcity. That scarcity is leading to inflation. Government funding through favorable tax treatment and investment is further cause of inflation.

So, if Kevin Warsh wants to make a dent in inflation, he needs to kill the golden goose. This is where the dual mandate of stable prices and low unemployment compete for dominance. The unemployment rate is 4.3% today, indicating a strong labor market against the backdrop of rising inflation. This should be an easy call – raise interest rates and give a little on economic growth. In fact, the other indicators that hawks might usually point to – the U.S. Treasury 2-year yield and the Taylor Rule – also indicate that the “right” move is to raise interest rates. It’s not even that clear that a small hike in rates would be that detrimental to the AI buildout.

Still, there are three things that have typically caused recessions in the past: oil shocks, geopolitical conflicts, and Fed policy mistakes. We have two of the three currently. If you were in Kevin Warsh’s shoes, would you want to be the one who implemented the third and drove the U.S. into recession?

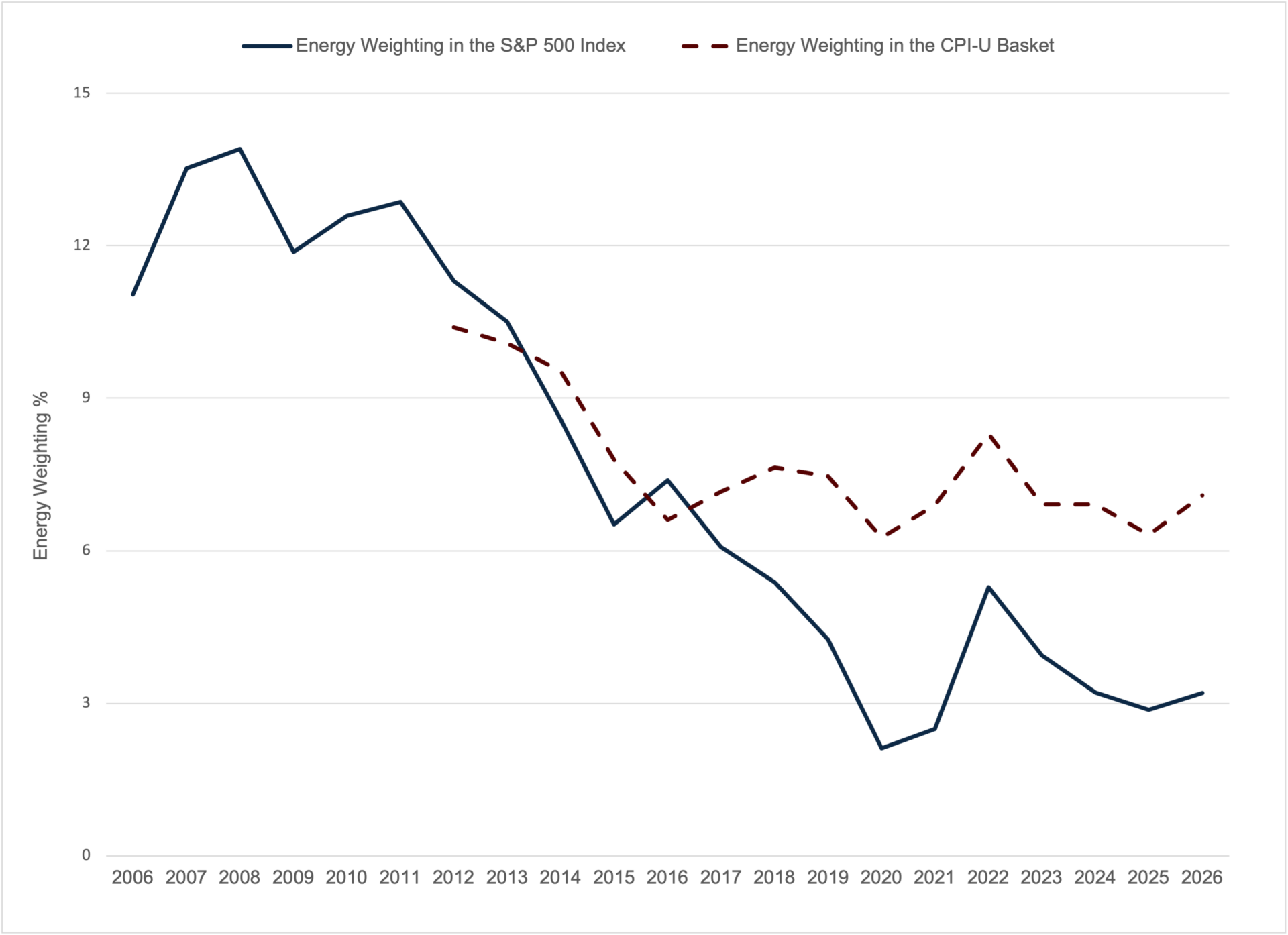

What do we do with this information? As believers in the AI story and investors up and down the supply chain, it seems like energy is an excellent barbell. Energy stocks have declined as a share of the S&P 500 over the past 20 years from 11% to 3%. At the same time, energy use has seemingly plateaued as a share of the CPI basket around 7%. The chart of the month displays this data.

Energy’s Weighting has Declined While Its Share of CPI Has Stabilized

Source: Bloomberg Finance, LP, Bureau of Labor Statistics

Our Energy overweight is based on three premises.

• Energy companies produce oil and gas at home for consumption by consumers at home, in transportation, and increasingly for data centers. A U.S. economy still in expansion requires more energy, not less.

• Domestic producers are increasingly important to the export picture supporting global supplies. Global supply disruption due to the Iran conflict has approximately halved from 20% to 9% per J.P. Morgan. This halving is due to re-routing, demand destruction, and strategic reserve releases. These offsets have mostly run their course and are more likely to reverse than remain static.

• Geopolitical analysis must consider that the Iranian regime (and U.S. foreign policy toward it) is likely to continue in joint militant intransigence. This stasis will ultimately result in a restart of hostilities (worst case) or a continued medium-term disruption of Middle East oil and gas supply like today’s balance (base case).

Should the war truly end, we would expect oil prices to come down, but the rest of our portfolios’ allocations would likely more than offset any sector decline before we could rebalance. The Fed and the economists may have the luxury of excluding food and energy, but we need to focus on the risks and opportunities provided by these crucial inputs and outputs.

Author

Gary Aiken

Chief Investment Officer

Concord Asset Management

Gary Aiken is the Chief Investment Officer for Concord Asset Management and is responsible for macroeconomic analysis, asset allocation, and security selection, as well as trading and investment operations.

Gary has over 23 years of investment experience and holds an undergraduate degree in economics from the University of Maryland and an MBA from The George Washington University School of Business.

—

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, including the investments and/or investment strategies recommended or undertaken by Concord Asset Management, or any non-investment related content made reference to directly or indirectly in this article, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. This content is provided for informational and educational purposes only and should not be construed as personalized investment, legal, tax, or accounting advice. Any forward-looking statements, opinions, or projections expressed herein are based on information available at the time of publication and are not guarantees, predictions, or assurances of future events, performance, or results. Actual outcomes may differ materially due to market conditions, economic developments, regulatory changes, changes in applicable laws or regulations, and other factors.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Concord Asset Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing.

Concord Asset Management is neither a law firm nor a certified public accounting firm, and no portion of this content should be construed as legal or accounting advice. A copy of Concord Asset Management’s current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.concordassetmgmt.com. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please remember to contact the firm in writing if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, and/or revising our previous recommendations and/or services, or if you would like to impose, add, or modify any reasonable restrictions to our investment advisory services. Concord Asset Management and Concord Wealth Partners shall continue to rely on the accuracy of information that you have provided.

Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please advise us if you have not been receiving account statements, at least quarterly, from the account custodian.