By Gary Aiken | March 5, 2026

Human emotion has sustained us since the first man or woman had to decide what to do when face to face with a saber tooth tiger. Fight or flight? That emotional instinct is what propels us forward and pushes us backwards as individuals and society. Progress needs logical inference and the scientific method as well. We can’t just depend upon our emotions and that is true in investing as well.

It is difficult though. How we view the world around us colors the way we see investment opportunities and how we interpret the data in front of us. I see this through the lenses of our clients who do not manage money for a living.

Our clients in the Washington, DC area saw firsthand the haphazard and insensitive DOGE cuts last year. They shared their emotional response (fear, frustration, anger) with our advisors and they asked if they should change their investment approach as a result. We responded that the data supported being long financial assets through our 2025 investment thesis: “the Grind”.

Our clients in southwestern Virginia shared anecdotes of industrial expansion as the AI boom demanded more steel, energy, and physical assets for data centers. They were bullish on America (hope, excitement, confidence). Still, we reiterated that it was time to sell US stocks and dip into international equities even though the latter had underperformed for the better part of the prior two decades. The world started to agree with our thesis – lower volatility, lower dollar, lower valuations formed the basis for international outperformance.

Recently, clients in Minnesota have started to share their emotions with our local advisors there. Who can blame them? Federal officers were deployed into their community and killed two civilians in a bad replay of Kent State in 1970. A few major employers announced layoffs for the first time since before the pandemic. For those clients, civil unrest, inflation, and unemployment loom large – fear, loathing, depression. But what does the data say?

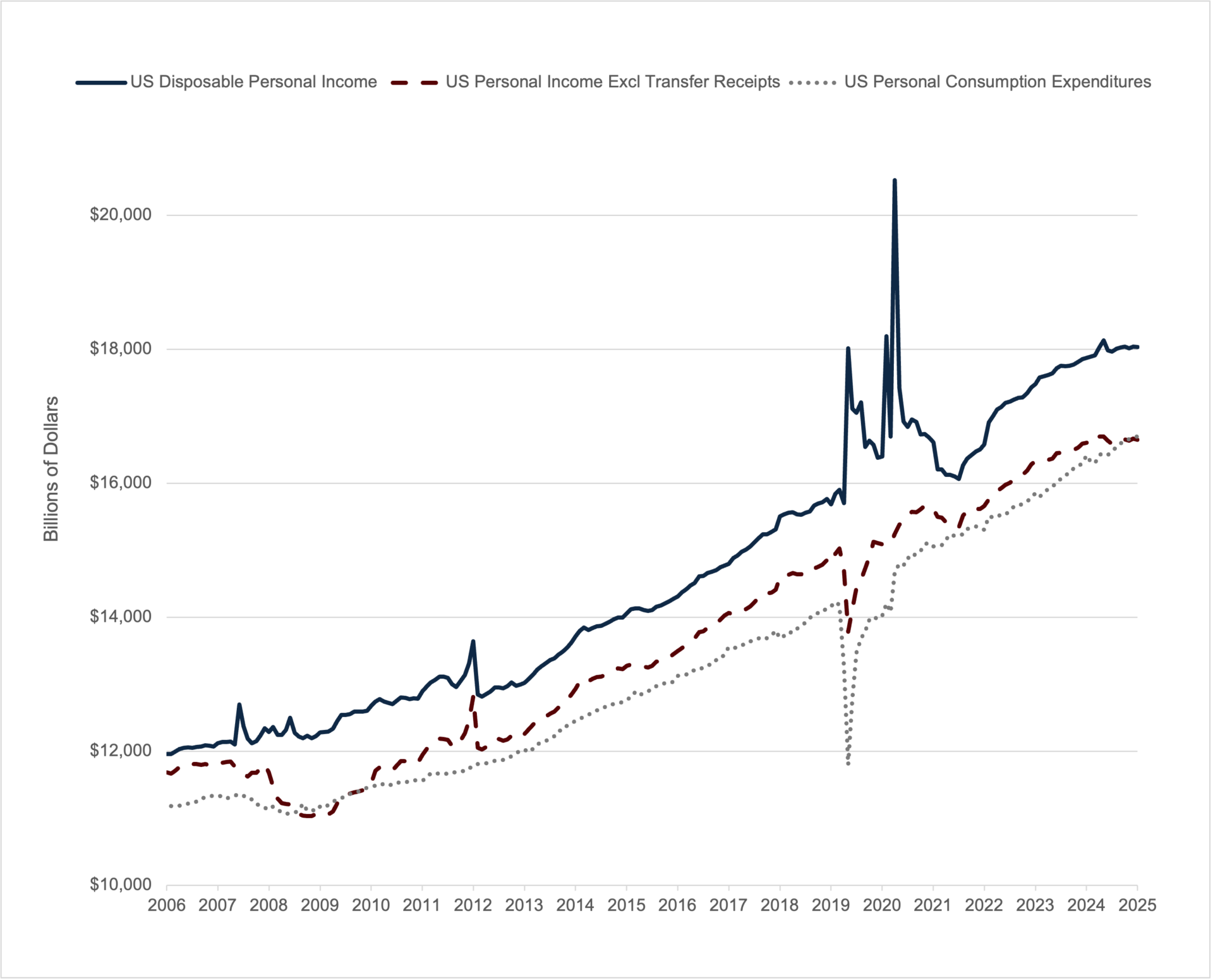

The Price Level is Above Incomes

Source: Bureau of Economic Analysis, Bloomberg Finance, L.P.

My chart of the month shows data that backs up the feeling of many Americans struggling to get by. It’s not the 4.2% unemployment rate, the empirically stagnant (and low) level of continuing unemployment claims, or the statistical fact of CPI below 3% and “truflation” even lower. When Americans go to the grocery or anywhere else, they’re confronted by the fact that prices just aren’t going down. Cumulative inflation – the price level – matters. That is shown as the US Personal Consumption Expenditures (PCE) Index used primarily by the Federal Reserve in thinking about the cost of living.

Further, wages have not kept pace.Incomes, excluding transfer payments from the government, are below the consumer price level. Americans feel bad about the economy and inflation. It is an emotional response in polling. It is also a rational response corroborated by data.

The last time incomes excluding transfer payments was below the price level was 2009-2010 – immediately following the financial crisis. The country was starting to heal, but it didn’t matter because so many Americans were out of work. For many, it felt like the government wasn’t working for them. The Tea Party movement grew out of this environment and elected the biggest shift in Congress (7 Senate seats and 63 House seats changed hands) since 1948.

Today, the public doesn’t trust Democrats or Republicans on inflation. President Trump is repeating President Biden’s mistake insisting that prices are coming down. They aren’t and anyone who spends money (everyone) knows it. Prices are still going up – they just aren’t going up as fast as they were a few years ago. That story, while true and healthy, doesn’t feel good.

We shouldn’t want prices to come down. Deflation is a spiral in which people decide to put off making a purchase or investment today, because they think they’ll get a better deal tomorrow. When enough people do this, economic activity slows down and prices do go lower. But that doesn’t encourage more activity – it reinforces the idea that waiting pays. The more we wait; the more prices go down. But less activity means fewer jobs and less ability to pay even at lower prices. That is deflation and depression.

What we want and need is more economic activity, a more productive workforce, and higher real wages. The good news is that we are seeing those things in the data: rising productivity, lower unemployment, and an increase in the labor force participation rate. Rising real wages should follow – as they did in 2018 and 2019 before the pandemic. The question for the Republicans seeking re-election is will this happen in time for the November election – when will the marginal voter feel better?

For our clients in Minnesota and beyond, my contention is that our investment thesis “the Grind” persists. The AI boom is in the mid-innings and productivity from AI will be incredibly bullish for US stocks. Still, volatility in the US will be elevated, the dollar is likely to continue to decline versus other major currencies, and lower valuations abroad are attractive and attracting our attention. In bonds, the economy is doing well and defaults for investment grade bonds are low. We think this is an environment that supports lower short-term rates and higher long-term rates. Fight or flight? Neither, unemotionally rebalance between the two as value and price dictate.

If you have any questions about your current investment strategy, please reach out to your Concord advisor. We welcome the conversation.

Author

Gary Aiken

Chief Investment Officer

Concord Asset Management

Gary Aiken is the Chief Investment Officer for Concord Asset Management and is responsible for macroeconomic analysis, asset allocation, and security selection, as well as trading and investment operations.

Gary has over 23 years of investment experience and holds an undergraduate degree in economics from the University of Maryland and an MBA from The George Washington University School of Business.

—

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Concord Asset Management, or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Concord Asset Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Concord Asset Management is neither a law firm, nor a certified public accounting firm, and no portion of this content should be construed as legal or accounting advice. A copy of Concord Asset Management’ current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.concordassetmgmt.com. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please remember to contact the firm in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, and/or revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Concord Asset Management and Concord Wealth Partners shall continue to rely on the accuracy of information that you have provided. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.