Key Observations:

- Equities experienced their first monthly losses since January with broad, deep declines.

- New supply chain challenges come front and center as a major headwind.

- Market pullbacks of 5% and greater are more common than you think.

A September to Forget

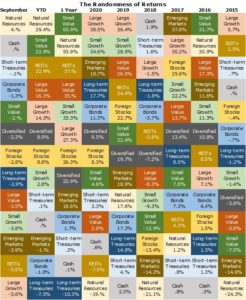

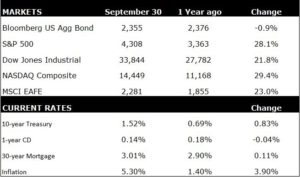

September has historically been the worst month of the year for equities, and it certainly lived up that reputation this year. Stocks finally sold off after seven consecutive months of positive returns. The Dow Jones, S&P 500, and NASDAQ 100 indices declined 4.2%, 4.7%, and 5.7%, respectively. The selloff was broad with few bright spots. According to Morningstar, 10 of the 11 economic sectors declined for the month. The lone bright spot was energy, up 9.8%. From large growth to small value, every asset class declined in September. How about foreign stocks? After trailing the performance of U.S. stock for eight straight months, developed market equities outperformed U.S. stocks by 1.75% as they declined “only” 2.9% in September. Emerging market stocks were less impressive, losing approximately 4.0%.

Losses were not isolated to the stock market. Bonds fared better but were still down as the Bloomberg US Aggregate Bond Index lost 0.9% in September. On the heels of a modest increase in longer-term yields, long-term Treasury bonds declined 2.9% while short-term bonds were flat. Oddly enough, junk bonds eked out a 0.02% return in what otherwise was a risk off-market. Lastly, precious metals failed to shine as gold dropped 4.0% and silver an incredible 10.5%.

Cause and Effect

What led U.S. stocks to experience their worst month since March of 2020? Most likely, it’s a confluence of several factors. Supply chain issues have come front and center once again. According to Business Insider, Southern California ports are experiencing their greatest ship-backlog on record. (1) As of the end of September, more than 65 enormous container boats were anchored off the Southern California coast while 95 massive cargo ships and another 147 vessels were in port, all records. The consequences include the average wait time for these vessels to unload has increased 40% from 6.2 to 8.7 days, the average time for an ocean freight to go door-to-door has increased 43% (50 days to 72 days), and the costs of shipping containers have risen by some estimates as much as 500%. Why does this matter? Stocks have performed consistently well this year with muted downside volatility because corporate earnings have smashed all expectations. These Southern California ports facilitate nearly 50% of all U.S. imports. Delays in delivering products to market and associated rising costs (and at the worst possible time as inventories need to ramp up for the Christmas season) have tamped down expectations earnings surprises will continue.

There’s more. Inflation pressures are not limited to supply chain issues. Labor remains in high demand and tight supply. We are all feeling the pain at the pump as oil has hit a seven-year high. (2) Inflation expectations are running hot even if bond yields are stubbornly range-bound. As many investors expect a significant increase in bond yields on the horizon, the appetite for high P/E technology stocks has disappeared.

Lastly, there is an even heightened risk to the seemingly endless stimulus from monetary and fiscal policy. Following September’s Federal Open Market Committee meeting, Fed Chairman Powell stated, “While no decisions were made, participants generally viewed that so long as the recovery remains on track, a gradual tapering process that concludes around the middle of next year is likely to be appropriate,” (3) Translation, the Fed is going pump the brakes on bond-buying to slow the growth in money supply.

As for fiscal policy, we have all witnessed the calamity in Washington as a once certain infrastructure bill, and its long-term economic impact is in peril. As these additional uncertainties were piled onto a near perfectly priced market, investors took profits and demanded greater expected returns from equities which required a decline in stock prices.

Final Thoughts – A Silver Lining

Yes, there are multiple reasons stocks slid sharply in September. However, it is worth noting profit-taking and the two most impactful headwinds, supply chain backlogs and inflation, are the result of a robust economic recovery led by strong aggregate demand. Recession is not in the cards, so a sustained bear market is highly unlikely. These 5% to 10% selloffs are however common in sustained bull markets. In fact, during the past ten years, the S&P 500 has experienced 18 selloffs of 5% or more during an eight-week period. (4) Taking profits and repricing risks are a normal part of a healthy stock market.

At CAM, we are constantly watching and assessing market conditions. If our long-term outlook changes, we will prudently adjust client portfolios to address our view of these opportunities and risks. Therefore, months like September are a good reminder to review your portfolio with your Advisor to ensure you have a well-diversified portfolio of stocks and bonds that will serve your financial planning needs.

Author

Mitch York

CIO

Sources:

All performance data is generated through Morningstar.

- https://www.businessinsider.com/largest-us-port-breaks-multiple-record-cargo-ships-import-delays-2021-9

- https://www.wsj.com/articles/opec-russias-gradual-oil-hike-pushes-prices-to-seven-year-high-11633356803

- https://www.cnbc.com/2021/09/22/watch-jerome-powell-speak-after-fed-wraps-up-september-meeting-live-blog.html

- https://www.cnbc.com/2021/10/04/op-ed-never-mind-the-headlines-a-decline-in-the-sp-500-could-present-an-opportunity.html

You cannot invest directly in an index. A description of each comparative benchmark/index is available upon request.

Disclaimer: Concord Asset Management, LLC (“CAM” or “IA Firm”) is a registered investment advisor with the Securities and Exchange Commission. CAM is affiliated, and shares advisory personnel, with Concord Wealth Partners. CAM offers advisory services, including customized sub-advisory solutions, to other registered investment advisers and/or institutional managers, including its affiliate, Concord Wealth Partners, LLC. CAM’s investment advisory services are only offered to current or prospective clients where CAM and its investment adviser representatives are properly licensed or exempt from licensure.

The information provided in this commentary is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All data is as of the end of April 2021 unless otherwise noted. Data sources include www.morningstar.com. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CAM or its affiliates, or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from CAM or CWP. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. IA Firm is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of IA Firm’s current written disclosure Brochure discussing our advisory services and fees is available upon request or at https://concordassetmgmt.com/. Please Note: If you are an IA Firm client, please remember to contact IA Firm, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. IA Firm shall continue to rely on the accuracy of the information that you have provided. Please Note: IF you are an IA Firm client, Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.