By Gary Aiken | July 9, 2026

Another day, another “A”. That was the motto in our household growing up. Despite the cheeky and easy-going feel of the phrase, getting to that result was anything but simple. Getting good grades, even for those who make it seem effortless, requires a lot of hard work behind the scenes. This sentiment is relayed by all those who achieve success from invention: “I am a great believer in luck, and I find the harder I work the more I have of it” – Thomas Jefferson; to sport – “Hard work beats talent when talent doesn’t work hard” – coach Tim Notke; and even to country music “It costs a lot of money to look this cheap” – Dolly Parton. The first half of 2026 is a lot like that for investors as our theme from 2025 persists into 2026 – the Grind continues.

To evaluate the first half, we start with our prior assumptions. First, the U.S. economy (and global economy) is in good shape; there’s no recession on the horizon. U.S. GDP for the first half of the year will come in likely between 2% and 2.5%, with inflation between 3% and 4%. That means nominal growth is between 5% and 6.5% (adding GDP in real terms to inflation). It’s definitionally impossible for a recession to exist in an environment where the economy is growing and hard to imagine when fiscal policies include large budget deficits and supportive tax policy.

Our second assumption was that the Federal Reserve was more likely to still be in position to ease than to tighten. We expected that if there were to be any rate decreases, they would be in the second half of the year. As predicted, the Federal Reserve held its main policy rate unchanged during the first half of the year, with the effective Federal Funds rate at about 3.63%. It’s important to understand that Fed policy has effectively become easier (less restrictive) as they have remained on hold at the same time measures of inflation have been rising. Their primary measure of inflation, the Core PCE Index, rose to its highest level in 3 years, 3.41%. The difference between Fed Funds and core inflation at 22 basis points (0.22%) is the smallest difference since the Fed ended its last hiking phase. Easy Fed policy is generally good for financial asset prices (at least in the short run).

Our third assumption moves us from “easy” to “hard” as my series of quotes to start this piece indicated. We named our strategic outlook “The Grind” because volatility would be with us again. Volatility came from two distinct places. First is geopolitics. The wars in the Middle East and Europe continued to escalate with Operation Epic Fury. Israel and the U.S., and later gulf allies eliminated the top echelons of Iranian leadership and inflicted serious damage to Iran’s capabilities to wage war. The Iranian regime, understanding the nature of the threat, responded by attacking not only Israeli and U.S. targets, but also attacking Arab gulf state oil, energy, and commodity infrastructure and effectively closing the Strait of Hormuz. This sent energy prices soaring and along with stock and bond volatility. Oil reached nearly $120/barrel in the futures market and much higher in the physical market. The VIX (a measure of U.S. stock volatility) reached 31 and the MOVE (a measure of bond volatility) reached 112 – both extreme levels. The U.S. and Israel backed off their most aggressive standpoints moving towards frameworks for longer term stability and markets recovered lost ground. Geopolitical risk extended volatility further into gold, interest rates, and currencies.

At the same time in the technology trade renewed fears of overbuilding and massive shortages competed during the first half of the year. We saw leadership in the stock market move from the hyperscalers and top chip makers to the suppliers in waves – neoclouds, memory makers, chip suppliers, energy providers, and AI infrastructure builders. If you don’t know what some of these words mean or have never heard of some of the biggest winners, that’s okay. Many long-term market participants also were surprised by the emergence of “left for dead” companies that found themselves the newest darling beneficiaries of the expanding AI buildout. These waves were like going into the ocean on a day at the beach. Sometimes the moves were small and manageable, but every now and then bigger than expected waves sent investors under the water and treading frantically to get back to the surface. Single stock volatility rose substantially during the first half of the year and made portfolio construction very important.

Our final assumption was that medium- and long-term interest rates were still more likely to rise than fall. Sticky inflation, healthy GDP growth, and reductions in the size of the Fed’s balance sheet were the main culprits. During the first half, the US 2-year rose 67 basis points (0.67%) from 3.47% to 4.14%. The 5-year, 10-year, 20-year, and 30-year yields also rose bringing bond investors price depreciation against their income leaving the major bond indexes virtually flat during the first half. The U.S. wasn’t the only place where yield rose though. Japanese, UK, and German yields rose similarly. This global parallel shift upwards in yields was a result of inflation and global geopolitics. Global investors sold local currencies and local currency bonds to buy U.S. Dollars.

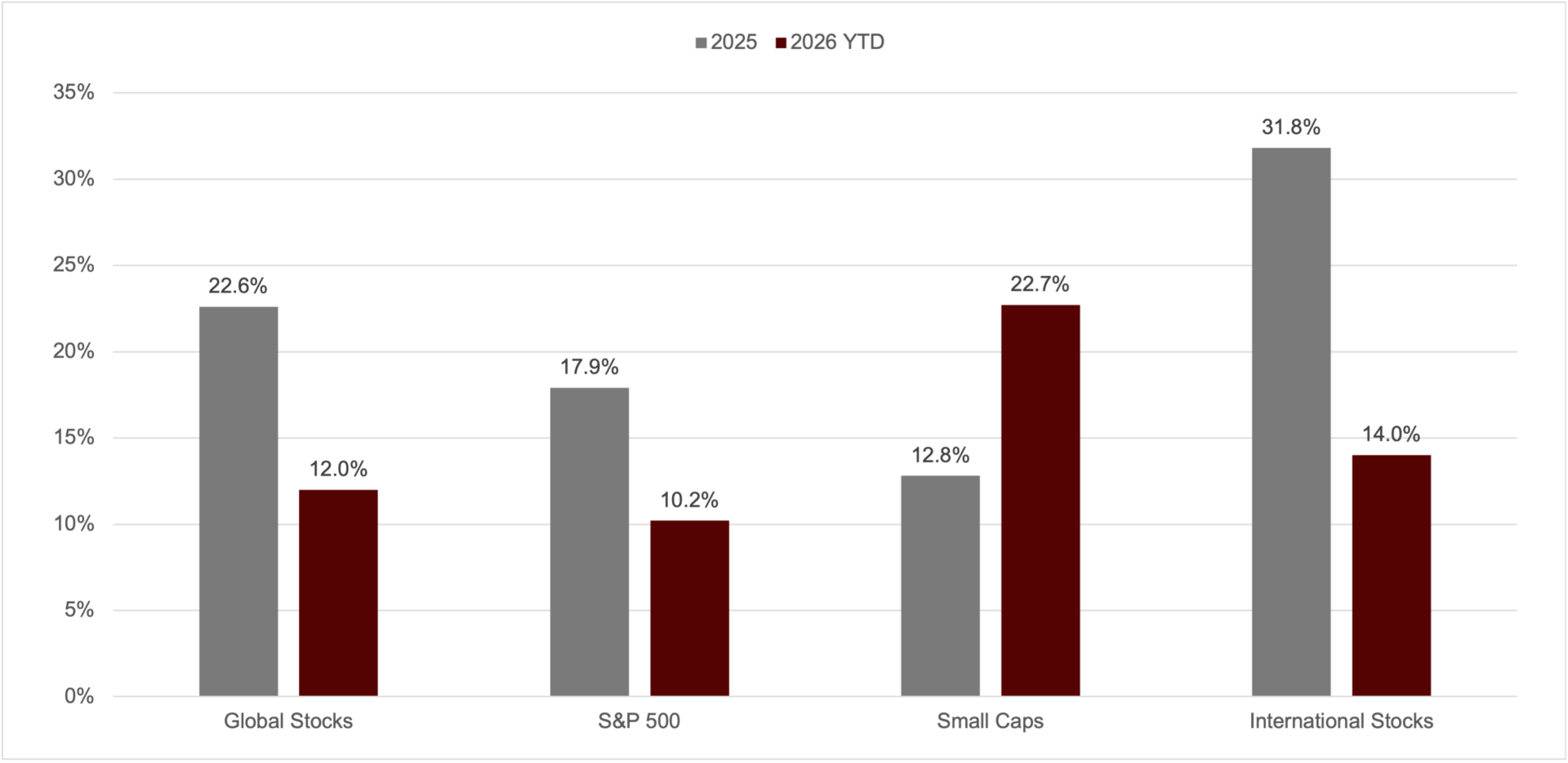

Total Returns in Global Stocks continued to be positive

Source: Bloomberg Finance, LP; data through 6/30/2026

Through all this turmoil and the proving of our major assumptions, the most important one for investors also came through. Global stock market prices ground higher. The chart of the month shows the performance of various stock markets. Global stocks were up 12% during the first half. The S&P 500 was up 10.2%, Small Caps rose 22.7%, and international stocks grew by 14%. The chart shows the previous year’s returns for these asset classes, too. Not for comparison, but rather to show that when the market fundamentals, the investment thesis, and underlying assumptions continue to be supported by facts on the ground, it’s important to do the hard work of remaining calm and invested. Did investors get another “A” during the first semester of 2026? Yes, but it was not easy, we earned success the hard way.

Author

Gary Aiken

Chief Investment Officer

Concord Asset Management

Gary Aiken is the Chief Investment Officer for Concord Asset Management and is responsible for macroeconomic analysis, asset allocation, and security selection, as well as trading and investment operations.

Gary has over 23 years of investment experience and holds an undergraduate degree in economics from the University of Maryland and an MBA from The George Washington University School of Business.

—

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, including the investments and/or investment strategies recommended or undertaken by Concord Asset Management, or any non-investment related content made reference to directly or indirectly in this article, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. This content is provided for informational and educational purposes only and should not be construed as personalized investment, legal, tax, or accounting advice. Any forward-looking statements, opinions, or projections expressed herein are based on information available at the time of publication and are not guarantees, predictions, or assurances of future events, performance, or results. Actual outcomes may differ materially due to market conditions, economic developments, regulatory changes, changes in applicable laws or regulations, and other factors.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Concord Asset Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing.

Concord Asset Management is neither a law firm nor a certified public accounting firm, and no portion of this content should be construed as legal or accounting advice. A copy of Concord Asset Management’s current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.concordassetmgmt.com. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please remember to contact the firm in writing if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, and/or revising our previous recommendations and/or services, or if you would like to impose, add, or modify any reasonable restrictions to our investment advisory services. Concord Asset Management and Concord Wealth Partners shall continue to rely on the accuracy of information that you have provided.

Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please advise us if you have not been receiving account statements, at least quarterly, from the account custodian.