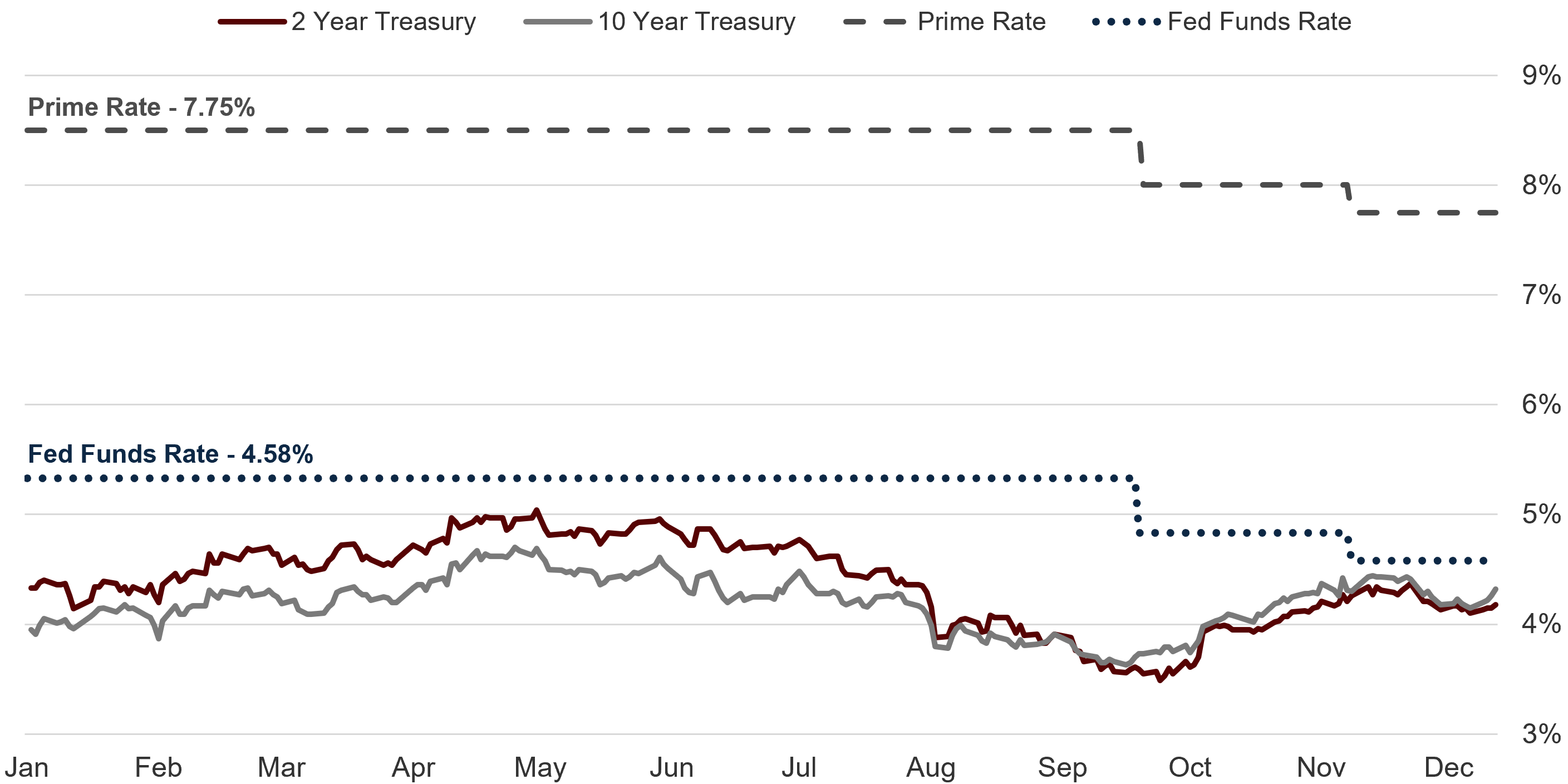

By Gary Aiken | March 6, 2025

President Trump announced a multitude of tariffs this week. To be clear, tariffs are a regressive tax on consumers that reduce overall trade, increase prices, and cost jobs. The mechanism of tax payments – while politically expedient – is less important than the decisions made by producers, consumers, and everyone else in the ecosystem of the products created and sold. In the military, there is a notion of “tooth-to-tail” ratios. For every soldier on the battlefield, there are many others in support roles, like the procurement officers, paymasters, and other military members who ensure that bullets and bread get to the front lines. This concept ignores those off-post – retailers, teachers, real estate agents, and others who support the military base. There are many more jobs supporting the warfighter than the number of warfighters.

The Trade Wars of 2018 impacted aluminum, airplane parts, batteries, cars, fruits, medical devices, nuts, pork, satellites, solar panels, soybeans, steel, televisions, weapons, and washing machines. While it sped up the timeline and importance of a revised NAFTA – USMCA – for increased cooperation between the United States, Mexico, and Canada, the Trade War did significant damage to the economies of both the United States and China. Each tariff trickles down through the economy.

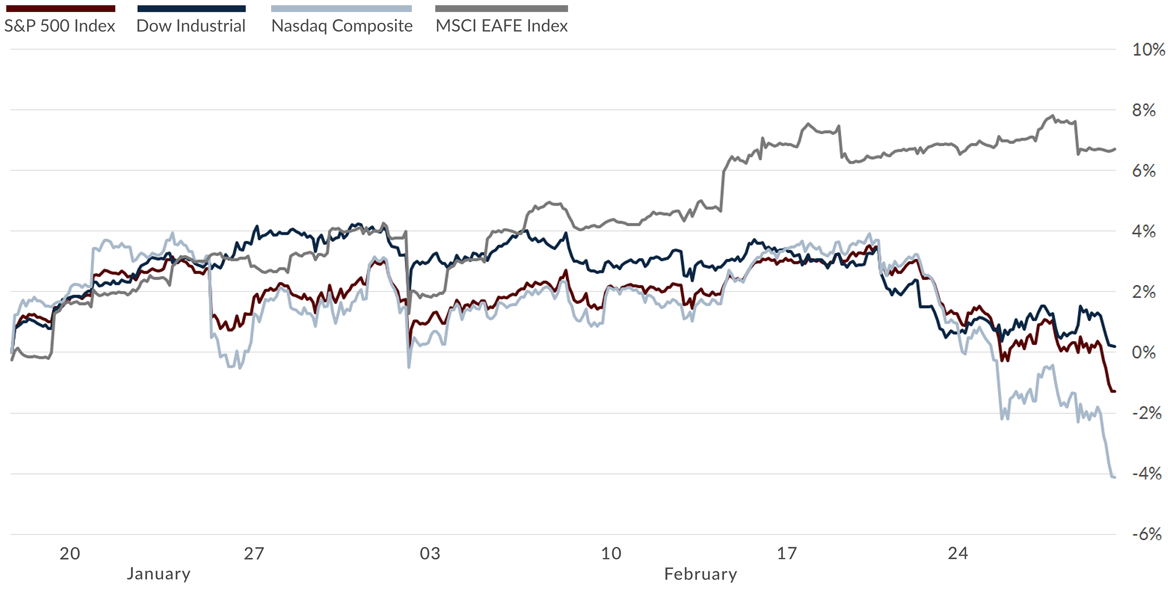

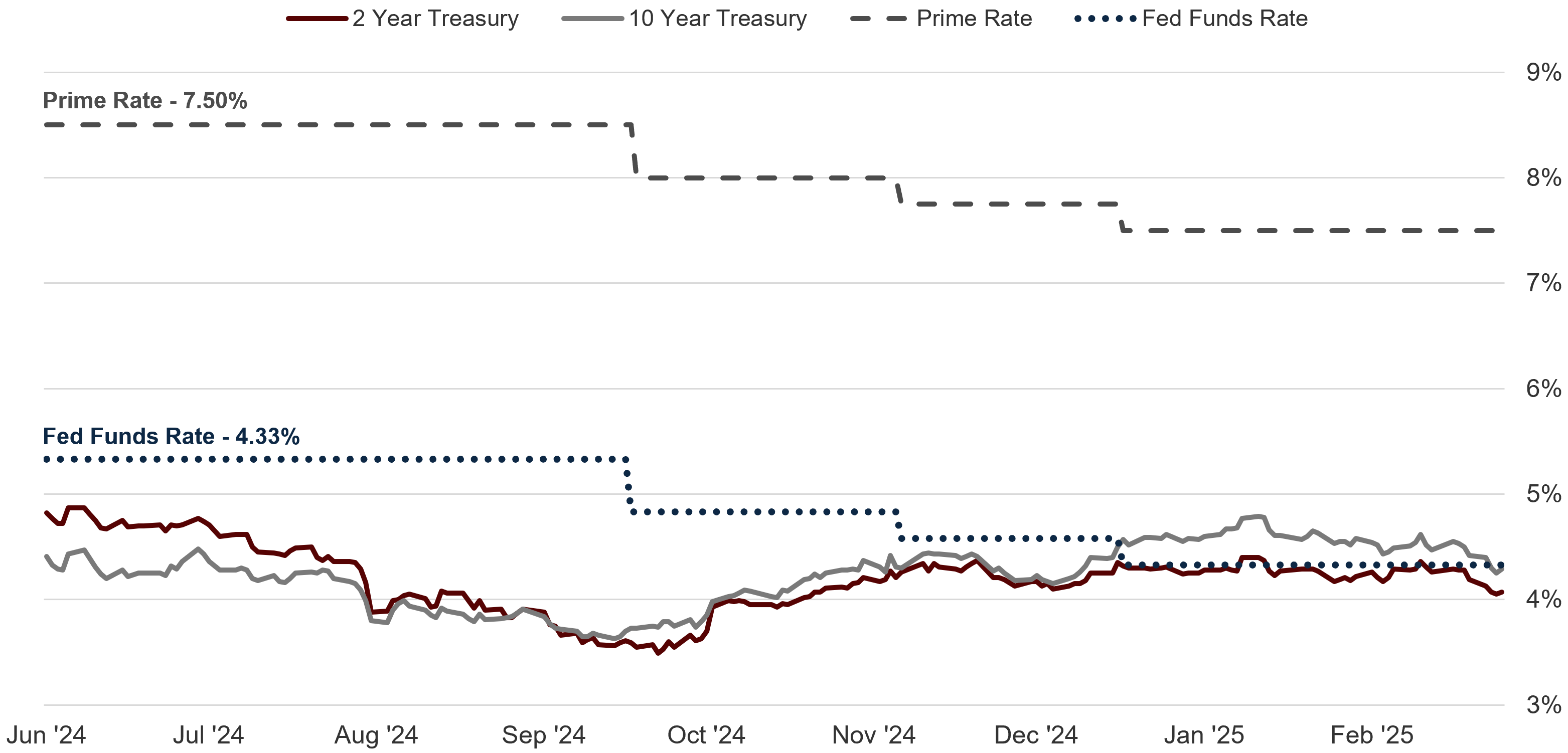

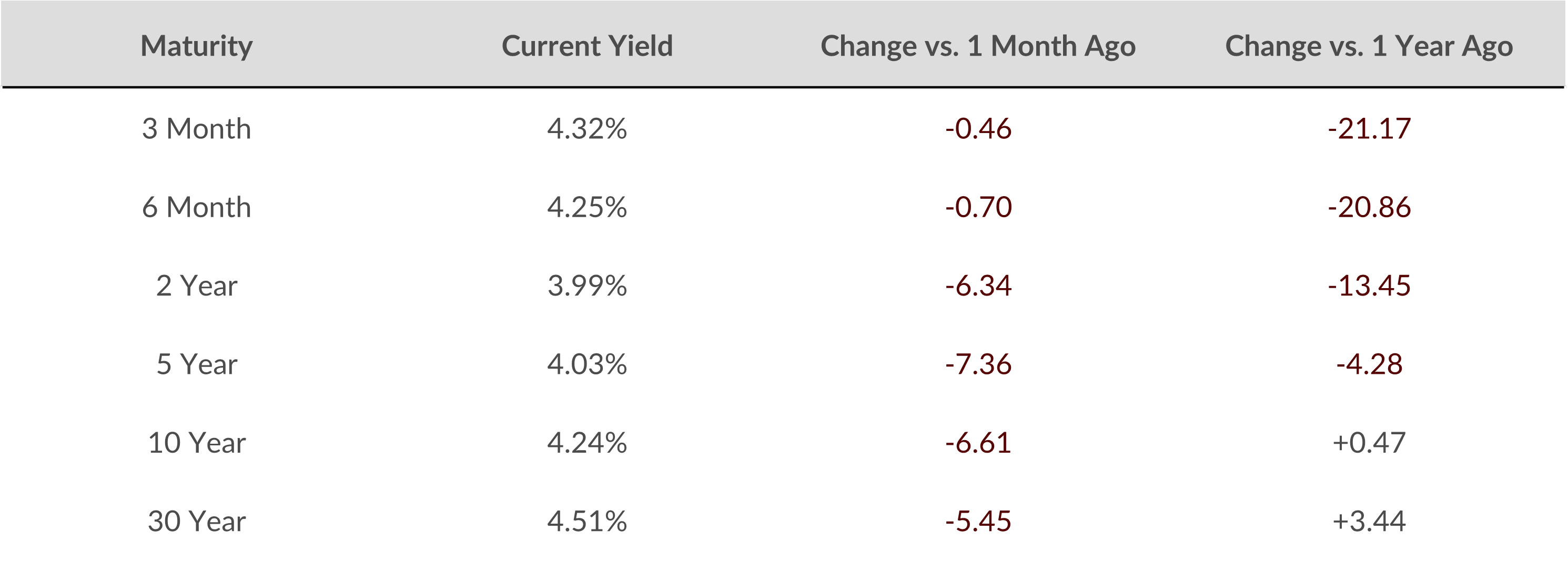

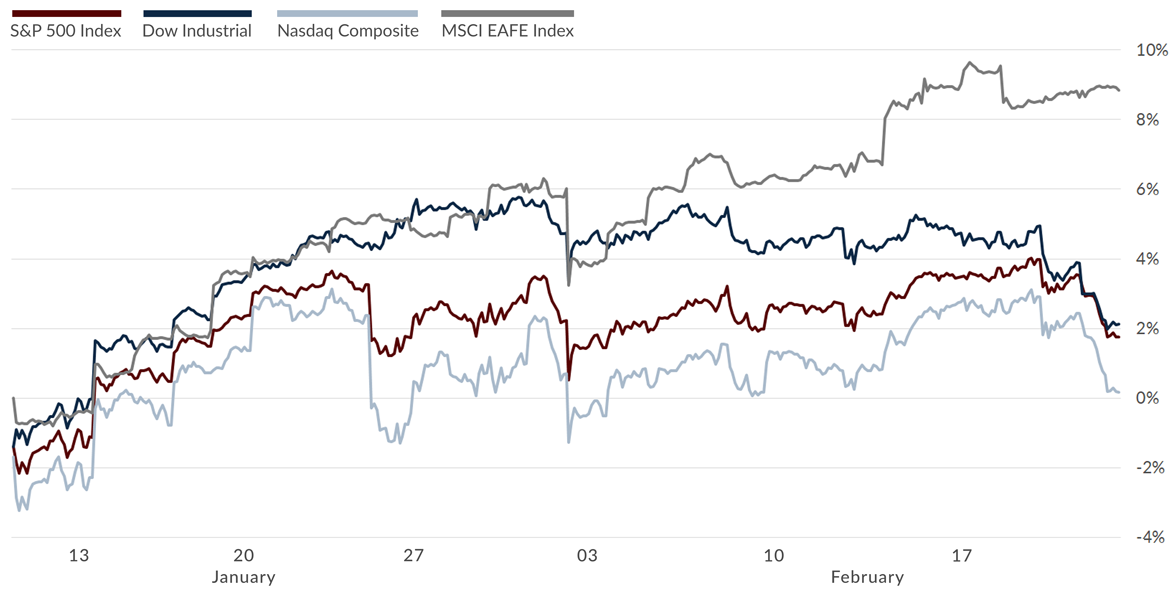

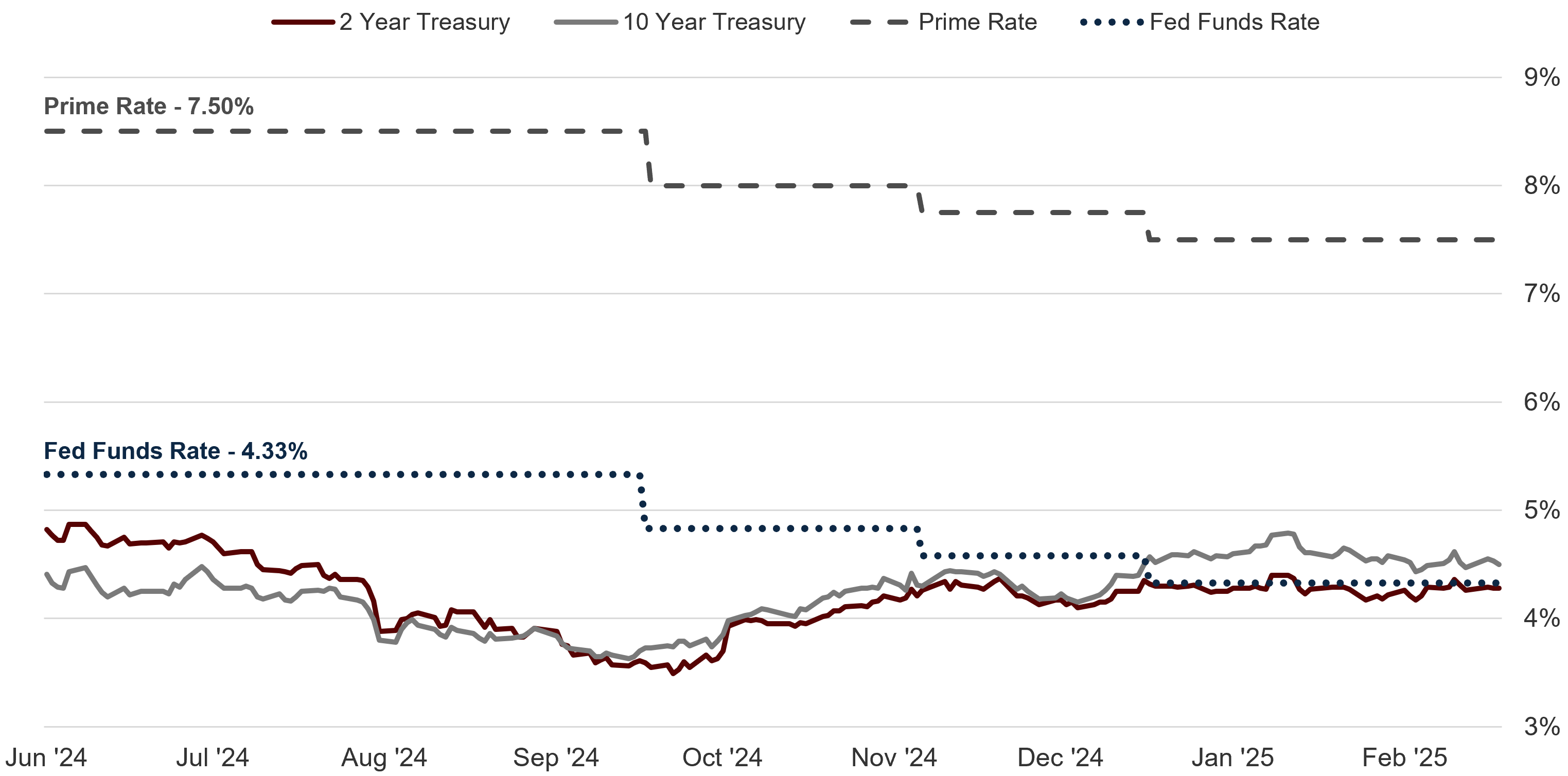

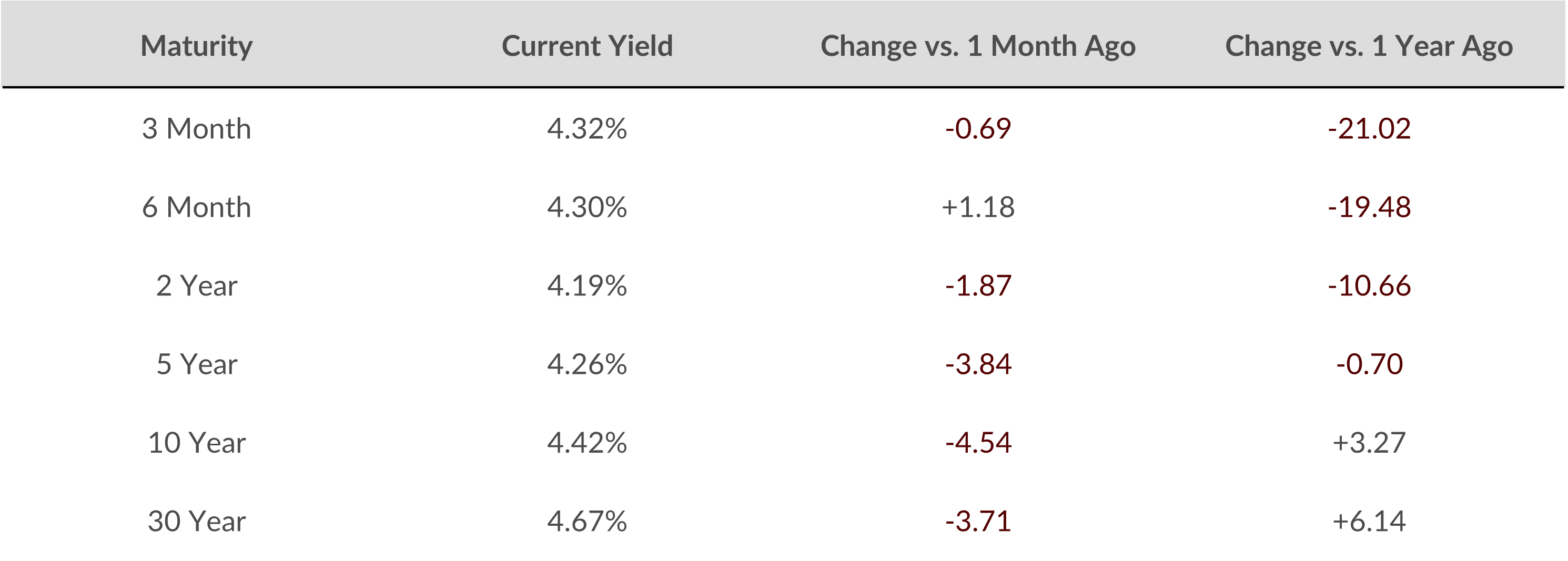

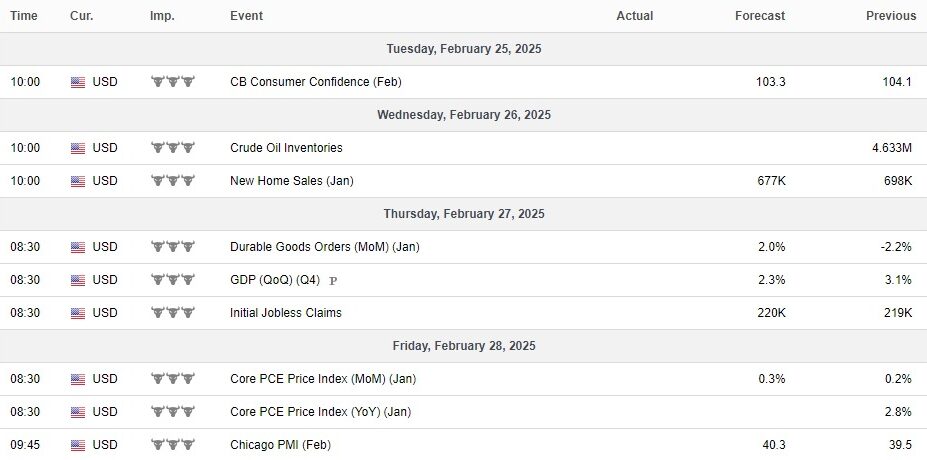

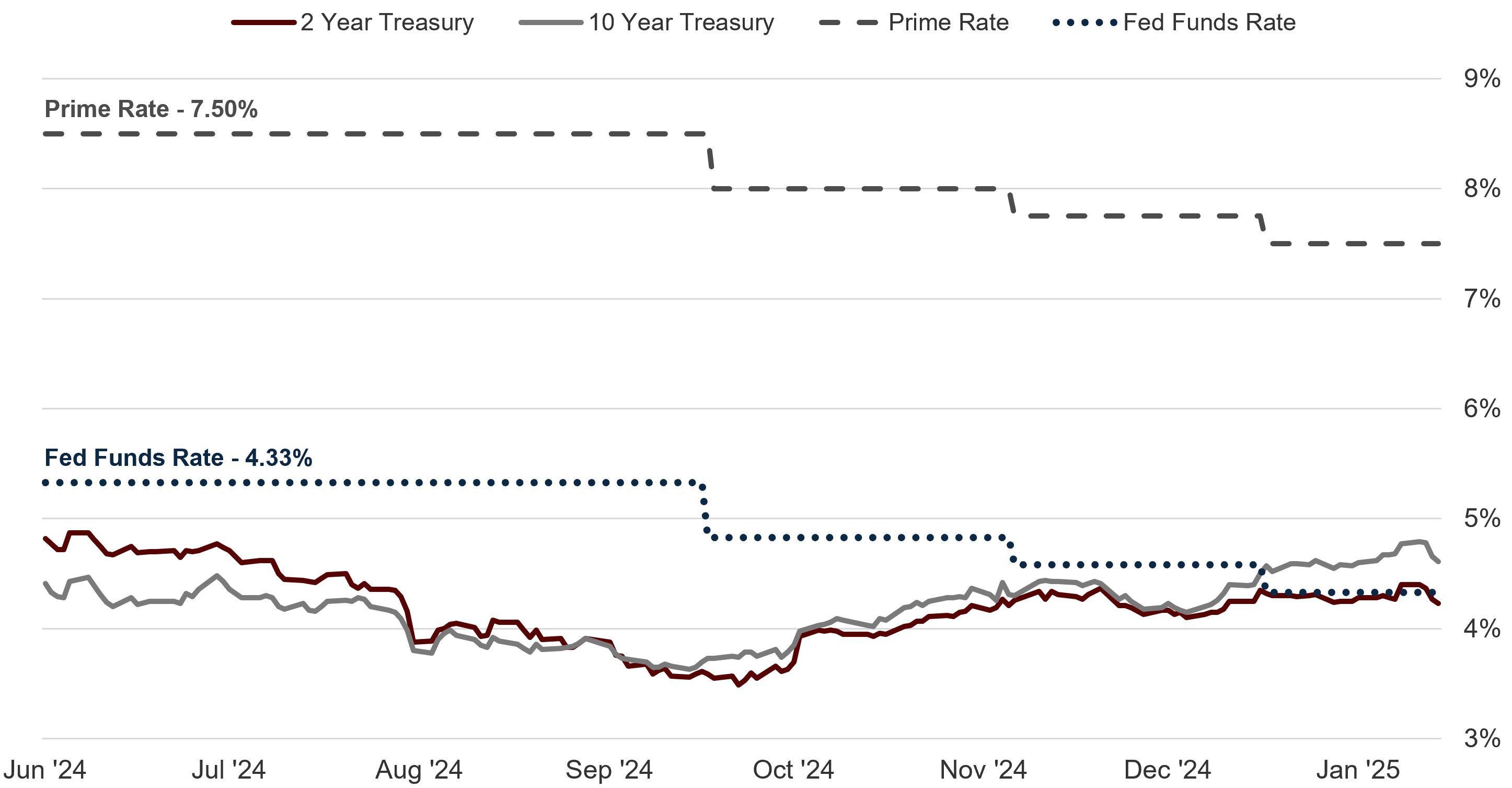

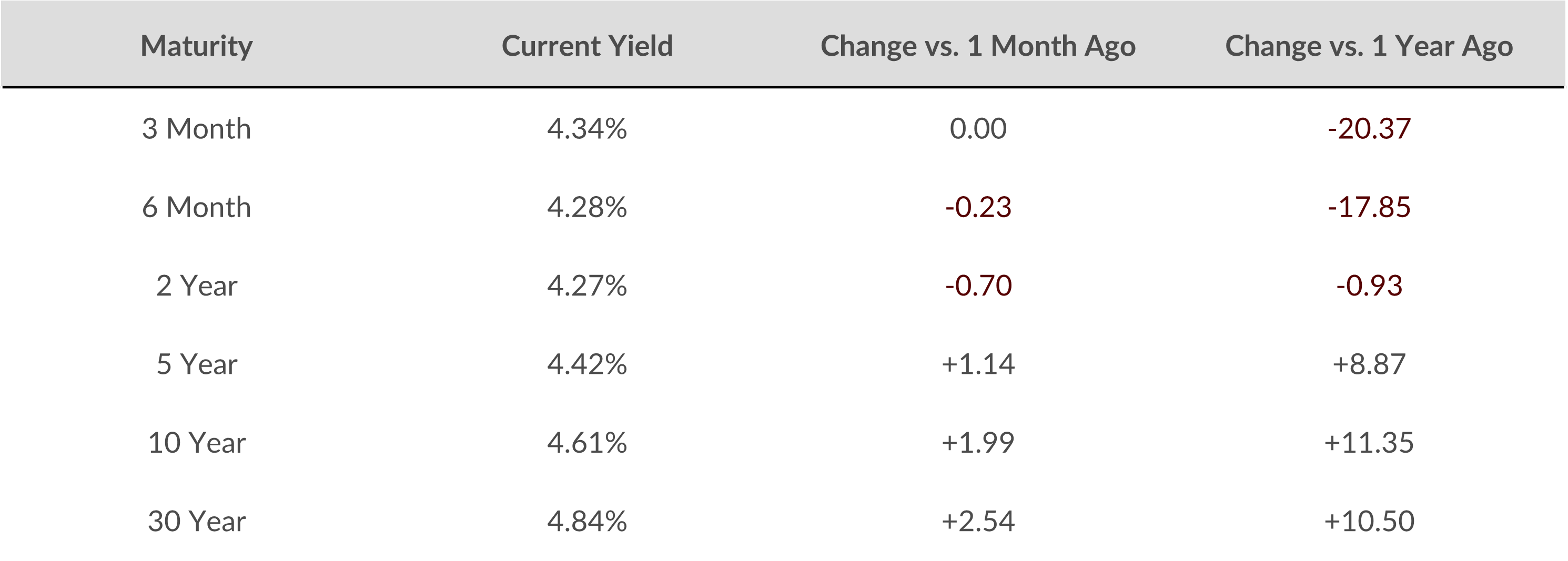

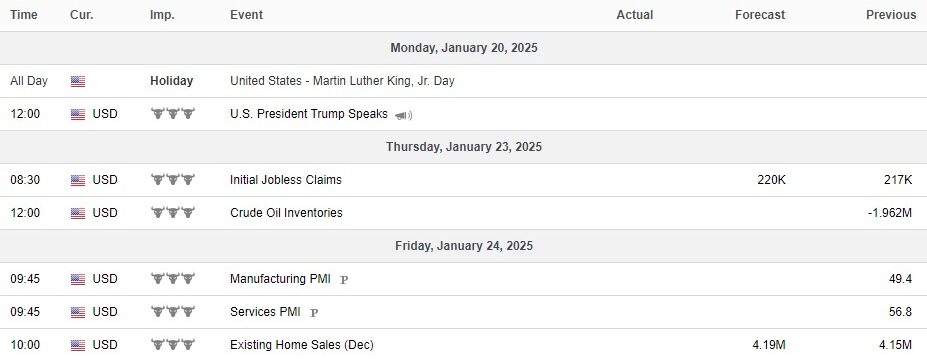

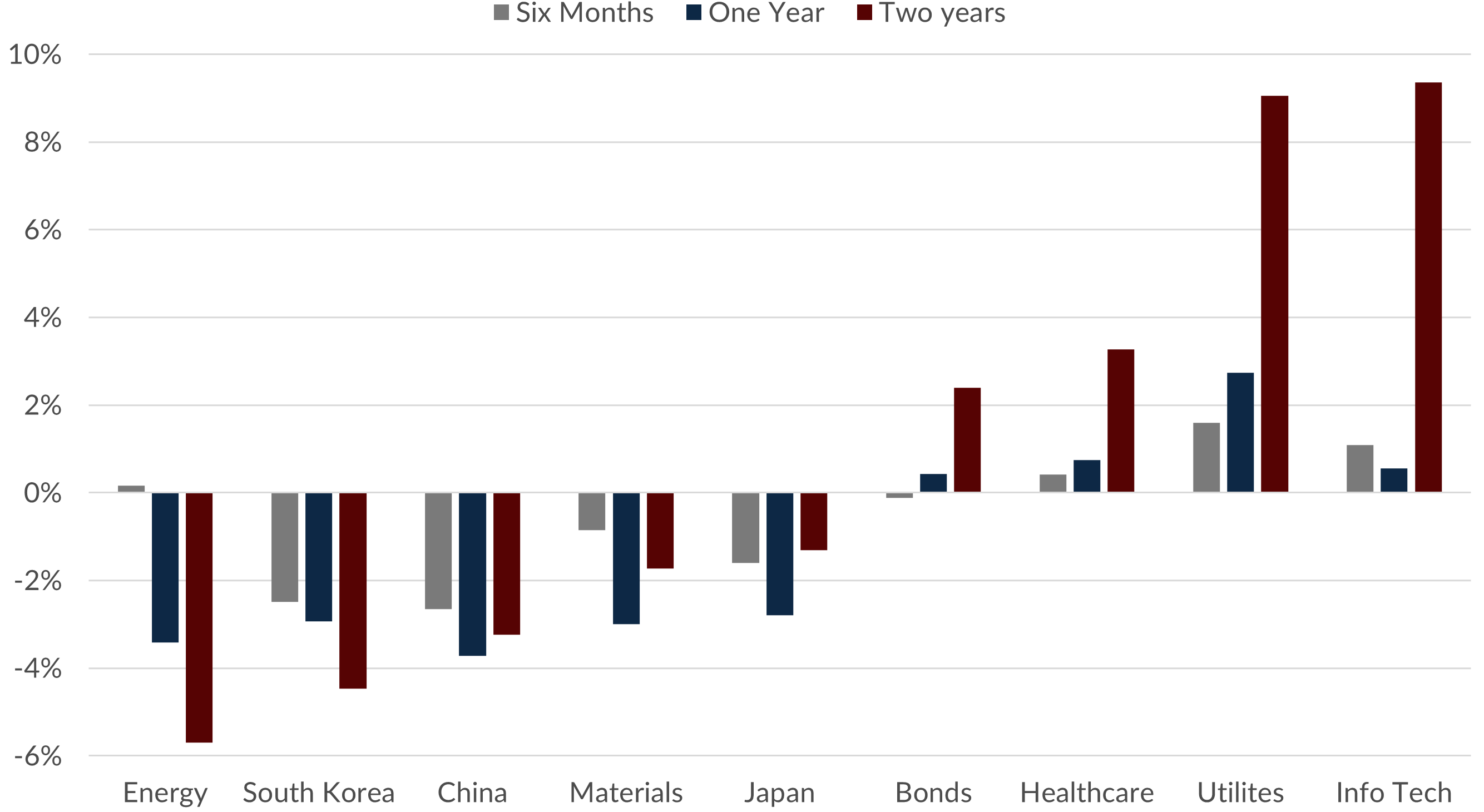

We suspect that the Trade War of 2025 will have similar effects on our economy and other combatants. The Trade War officially began on January 22, 2018. The chart below highlights some winning and losing market sectors for six months, one year, and two years following.1

Winners & Losers2

Sources: Bloomberg Finance, L.P.

A Trade War reduces economic growth. In that environment we might suspect that energy and other industrial commodities’ stocks might suffer. As economic activity slows, we use relatively less oil, iron ore, and copper. Profits and jobs tied to the price of a commodity decline.

It is no surprise that China was hit hard by the trade war, but countries that trade with China were also harmed, including South Korea and Japan. In fact, during the 2018-20 trade war, Emerging Markets and Developed Markets stocks both headed generally lower.

Brazilian stocks fared well during that trade war as they provided both agricultural and energy commodities to combatants trying to avoid the tariffs. Some observers think India could play a similar role in this trade war.

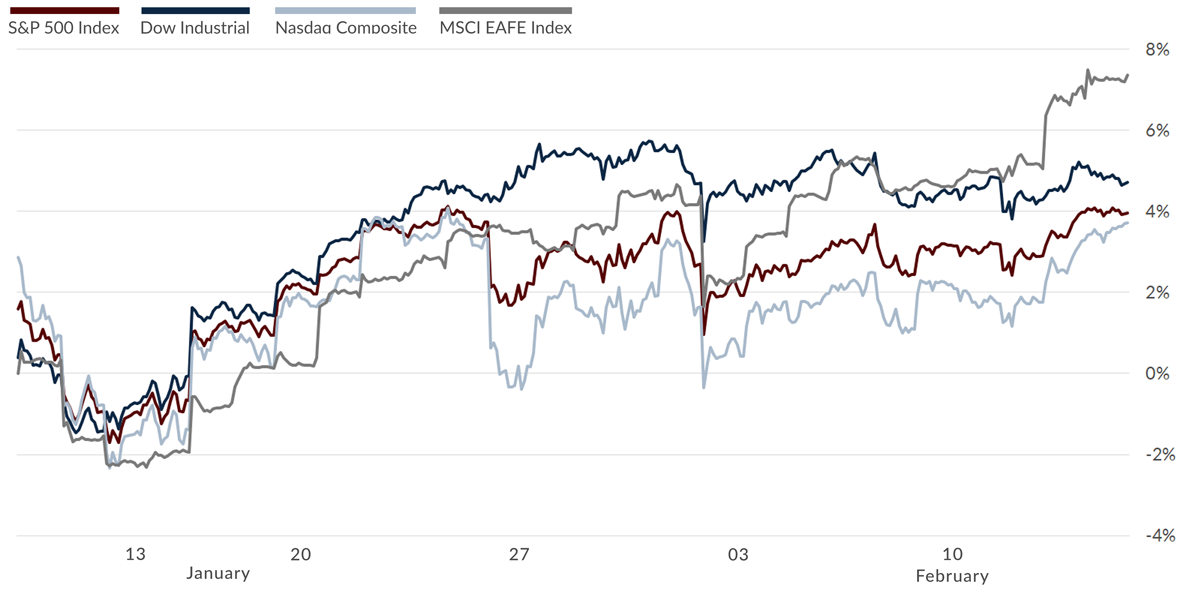

Growth stocks led U.S. stocks higher, and Utilities provided shelter from the storm. This barbell of risk and safety could certainly work out again, but as we warned in our 2025 Forecast, we expect that the high valuations to start the year may result in a draw down, providing better entry points for tech stocks later in the year.

President Trump and Chairman Xi inked a deal to start ending the trade war in January 2020. Interestingly, the deal included an out for a “natural disaster or other unforeseeable event.” COVID-19 emerged quickly thereafter. While glimpses into the past can prove instructive, let us hope that this Trade War has a happier ending.3,4

At Concord, we’ll keep a close eye on the developments of the Trade War of 2025 to ensure our clients are informed of any potential risks or opportunities. As the situation evolves, we aim to provide timely insights and strategies to help you navigate these uncertain times with confidence.

Author

Gary Aiken, Chief Investment Officer

Gary Aiken is the Chief Investment Officer for Concord Asset Management and is responsible for macroeconomic analysis, asset allocation, and security selection, as well as trading and investment operations.

Gary has over 21 years of investment experience and holds an undergraduate degree in economics from the University of Maryland and an MBA from The George Washington University School of Business.

—

Footnotes and Sources

1Ailworth, Jacob M. Schlesinger and Erin (January 23, 2018). “U.S. Imposes New Tariffs, Ramping Up ‘America First’ Trade Policy.” The Wall Street Journal.

2“Energy” refers to Vanguard Energy ETF, “South Korea” refers to iShares South Korea ETF, “China” refers to iShares China ETF, “Materials” refers to Vanguard materials ETF, “Japan” refers to iShares Japan ETF, “Bonds” refers to Bloomberg Aggregate Bond Index, Healthcare refers to Vanguard Healthcare ETF, “Info Tech” refers to Vanguard Info Tech ETF.

3Donnan, Shawn; Wingrove, Josh; Mohsin, Saleha (January 15, 2020). “U.S. and China Sign Phase One of Trade Deal.” Bloomberg.

4Suppan, Dr. Steve (March 27, 2020). “COVID-19 and US-China Trade and Investment.” Institute for Agriculture & Trade Policy.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Concord Asset Management, or any non-investment related content, made reference to directly or indirectly in this article will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this article serves as the receipt of, or as a substitute for, personalized investment advice from Concord Asset Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Concord Asset Management is neither a law firm, nor a certified public accounting firm, and no portion of this content should be construed as legal or accounting advice. A copy of Concord Asset Management’ current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.concordassetmgmt.com. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please remember to contact the firm in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, and/or revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Concord Asset Management and Concord Wealth Partners shall continue to rely on the accuracy of information that you have provided. Please Note: If you are a Concord Asset Management or Concord Wealth Partners client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.